This report will examine the structural rise of speculative behavior across modern society and financial markets. Over the past decade, and particularly following the post-COVID economic regime, speculation has increasingly evolved from a niche activity concentrated within casinos and financial institutions into a normalized component of everyday life. The ability to trade, gamble, leverage, and speculate on nearly any event or asset class now exists inside frictionless digital systems accessible to billions of individuals globally.

We will explore how technological infrastructure, mobile financial applications, social media, legalized sports betting, prediction markets, and twenty-four-hour digital markets collectively contributed to the normalization of speculation as both a cultural behavior and economic activity. Particular attention will be placed on the collapse of friction surrounding participation itself, where activities that once required physical presence, institutional access, or significant financial capital can now be executed instantly through a smartphone.

This report will also compare the current speculative environment against prior historical periods in order to better understand how society arrived at this point. We will examine how the gradual financialization and democratization of finance transformed participation in markets from a specialized activity into a mainstream social phenomenon increasingly embedded into entertainment, identity, and online culture. Modern gambling and brokerage platforms often describe this transition as expanding access and participation, but the resulting systems increasingly blur the distinction between investing, entertainment, and wagering.

Additionally, we will analyze the broader economic backdrop that incentivized speculative participation among consumers. Following years of asset inflation, rising housing costs, tuition inflation, weak wage progression relative to financial assets, and increasingly K-shaped economic outcomes, speculative behavior has become economically and psychologically attractive to many participants seeking asymmetric upside within systems where traditional upward mobility feels increasingly constrained.

Finally, after establishing where modern speculative culture originated and the structural forces driving its expansion, we will attempt to understand the implications of this transformation for both society and markets themselves. This includes examining how increasingly reflexive retail participation, narrative-driven positioning, and speculation-heavy flows may influence volatility, liquidity, and modern market microstructure dynamics going forward.

This report does not seek to moralize speculation itself. Rather, it seeks to understand why speculative behavior has become increasingly embedded into the structure of modern economic and social life.

The Collapse of Friction

The rise of modern speculative culture cannot be understood without first understanding how dramatically the friction surrounding financial participation has collapsed over the past several decades. Only a generation ago, both investing and gambling required meaningful effort, institutional access, physical presence, and financial capital. Participation itself carried operational barriers that naturally constrained speculative behavior to a relatively narrow segment of society.

In the 1970s and 1980s, participating in financial markets largely required direct interaction with brokers while commissions remained expensive and information traveled slowly. Real-time charts, instant execution, twenty-four-hour markets, and leveraged financial products were inaccessible to most ordinary individuals. Trading was operationally cumbersome and often viewed as something reserved for professionals, institutions, or wealthy investors.

The same was true for gambling. Sports betting was geographically constrained and frequently illegal across much of the United States. Casinos existed as isolated physical destinations rather than persistent digital ecosystems integrated into daily life. Participation required deliberate effort. A person needed to physically travel to a sportsbook or casino in order to engage in speculative behavior.

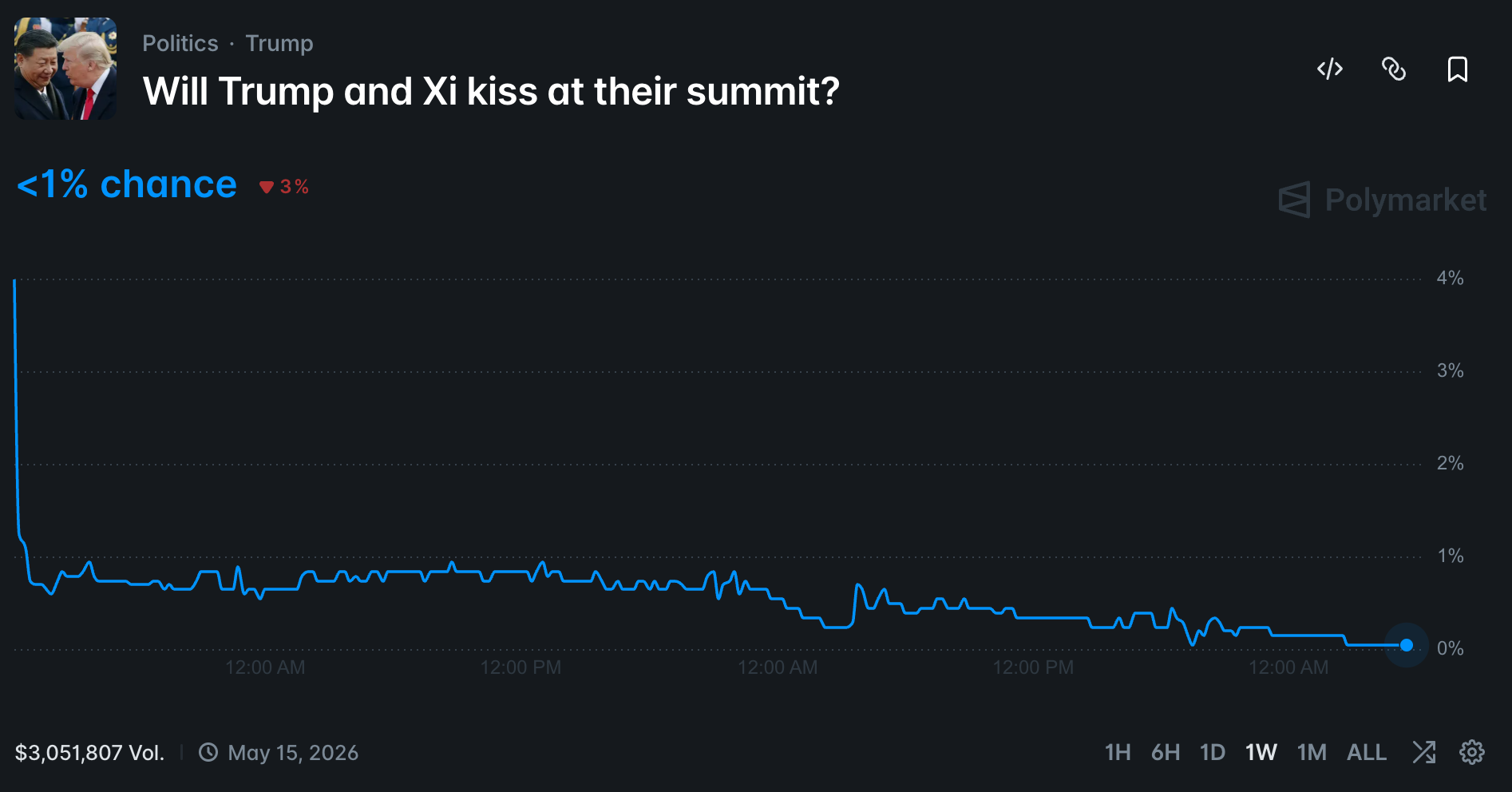

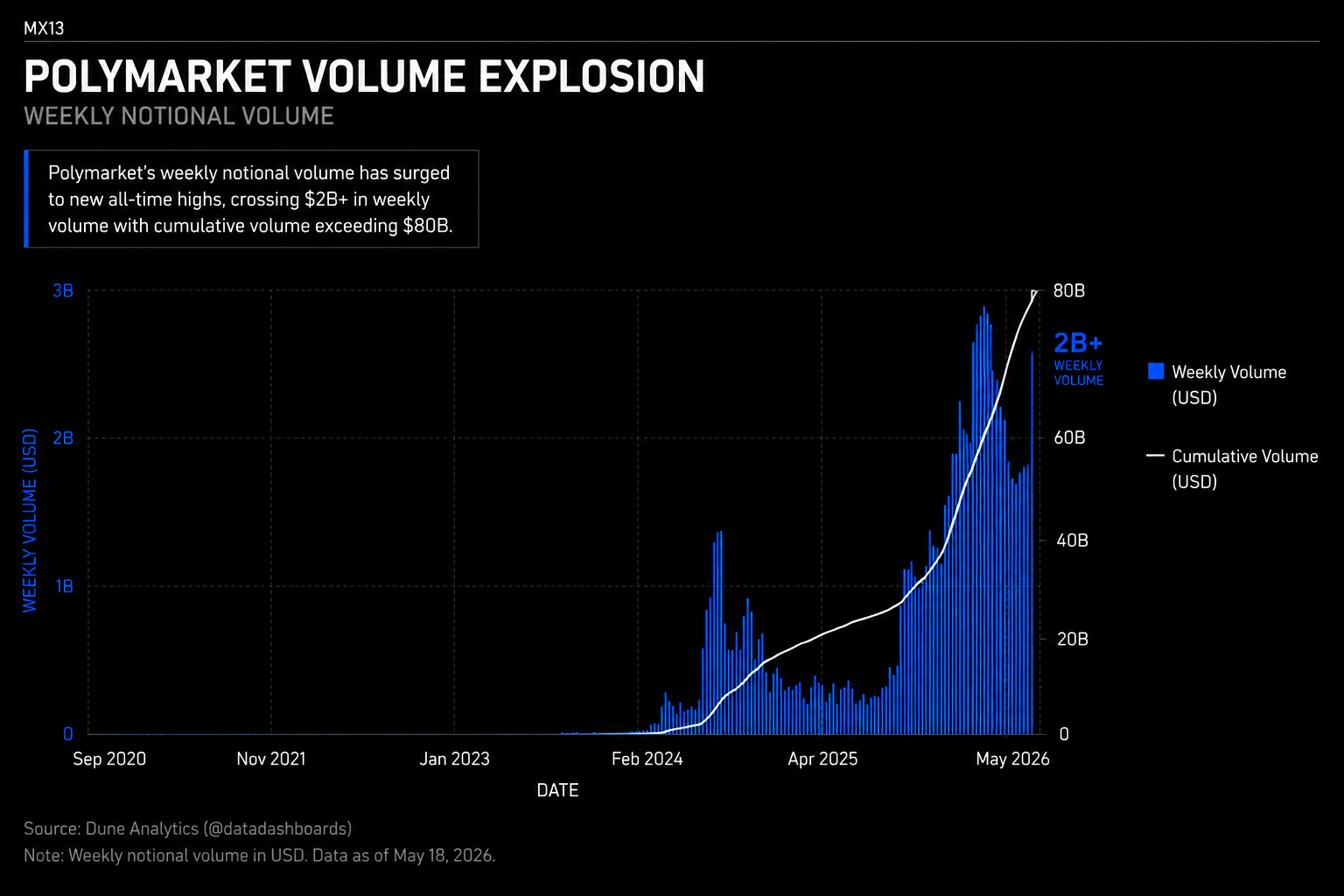

Today, nearly all of those constraints have disappeared simultaneously. A smartphone now provides immediate access to leveraged options trading, perpetual crypto futures, prediction markets, sports betting, memecoin speculation, and twenty-four-hour global financial markets. A user can purchase weekly call options on a semiconductor company, rotate into a memecoin launched six hours ago, place a same-game parlay during halftime, or trade whether Trump and Xi Jinping will kiss during their summit meeting.

The friction to speculate collapsed toward zero. Importantly, this transformation extends beyond accessibility alone. Modern speculative platforms increasingly optimize for engagement itself. Robinhood famously introduced gamified design structures including confetti animations, dopamine-driven notifications, simplified interfaces, instant deposits, and swipe-based trading mechanics designed to reduce psychological hesitation around participation. Trading increasingly began resembling entertainment rather than traditional financial decision-making.

This broader convergence between finance and wagering continues accelerating. Interactive Brokers now offers prediction markets directly within brokerage infrastructure, while multiple major financial platforms increasingly integrate event contracts and sports-related speculative products into traditional investment interfaces. The distinction between long-term investing and short-term wagering continues to weaken operationally, psychologically, and culturally.

An individual can now access their retirement account, buy leveraged technology exposure, and place a wager on an NBA game from the same application within minutes.

The internet effectively merged finance, gambling, entertainment, and social media into a single behavioral environment. This distinction matters because speculation no longer exists as an isolated activity detached from ordinary life. It has become ambient, persistent, and socially integrated into the structure of everyday digital behavior itself.

Ownership Outperformed Labor

While the collapse of friction explains how speculative participation became possible at mass scale, it does not fully explain why speculation became so culturally attractive in the first place. The broader macroeconomic backdrop following the Global Financial Crisis and post-COVID asset cycle played a critical role in shaping the incentive structure driving modern speculative behavior.

Over the past several decades, financial assets dramatically outperformed wage growth across much of the developed world. Equities appreciated substantially, housing prices surged, and ownership of financial assets increasingly became the dominant mechanism through which wealth compounded. Simultaneously, younger generations faced rising housing costs, tuition inflation, elevated debt burdens, credential inflation, and declining confidence in traditional pathways toward upward mobility.

Ownership increasingly outperformed labor.

This dynamic matters because societies often become more speculative during periods where financial assets compound materially faster than wages and productivity. The modern economic system increasingly rewards ownership rather than income generation alone. Individuals who owned homes, equities, businesses, and financial assets during the long-duration asset inflation cycle experienced enormous wealth appreciation. Younger generations entering adulthood later in this cycle inherited inflated asset prices, weaker purchasing power, and significantly higher barriers to ownership.

The divergence between generations is increasingly measurable across nearly every major economic category including home ownership rates, debt burdens, wage purchasing power, and asset ownership concentration. A generation ago, a single income household could often support home ownership, education costs, and family formation with materially lower debt burdens. Today, many younger workers graduate into expensive labor markets where housing affordability has deteriorated significantly, wages frequently lag major living expenses, and economic advancement increasingly feels dependent on financial asset exposure rather than labor progression alone.

Importantly, this dynamic is not simply accidental. Older generations collectively own the majority of financial and real estate assets across developed economies, meaning political and monetary systems increasingly become incentivized toward preserving asset values and delaying deleveraging events. Policy responses following both the Global Financial Crisis and COVID largely reinforced this structure through aggressive monetary intervention, liquidity expansion, and financial asset support mechanisms.

The result is an economy where younger participants increasingly observe that traditional progression compounds slowly while financial speculation offers the possibility of nonlinear upside.

Under these conditions, speculative behavior increasingly becomes economically rational from the perspective of many participants. If housing feels unattainable, wages lag living costs, education creates large debt burdens, and traditional career progression appears structurally weaker than prior generations, then participation in highly speculative environments naturally becomes more attractive psychologically.

This helps explain why younger generations increasingly gravitated toward memecoins, leveraged options, sports betting, prediction markets, perpetual futures, and highly speculative technology narratives. The hypergambling economy is not merely cultural. It is incentive-driven.

Importantly, modern information systems continuously reinforce this behavior socially. Social feeds display screenshots of overnight gains, viral trading success stories, and narratives surrounding individuals generating wealth through speculative positioning. Simultaneously, the visible costs of traditional milestones such as home ownership, education, and financial independence continue rising.

The result is a powerful psychological divergence where traditional economic progression increasingly feels constrained while asymmetric speculative upside appears normalized, socially reinforced, and increasingly necessary to achieve meaningful financial mobility.

The Infinite Casino

The cumulative result of collapsing friction, generational economic divergence, and digitally integrated financial infrastructure is the emergence of what increasingly resembles a continuous global speculative environment operating twenty-four hours per day across interconnected platforms.

Modern speculation no longer exists exclusively inside Las Vegas casinos or institutional trading floors. It exists simultaneously across sportsbooks, brokerages, crypto exchanges, prediction markets, livestreams, social feeds, podcasts, and online communities operating continuously at global scale. Participation itself increasingly feels less like entering a specialized financial environment and more like interacting with ordinary internet culture.

At the same time, the speed of narrative propagation accelerated dramatically. Information now moves through decentralized online systems where positioning, sentiment, and collective attention reinforce themselves reflexively through viral feedback loops. In many areas of the market, narrative velocity increasingly matters alongside traditional fundamentals as flows rapidly rotate between sectors, themes, and speculative opportunities.

Importantly, retail speculation itself increasingly concentrates around highly narrative-driven areas of the market rather than traditional macroeconomic instruments. Retail participants generally do not trade interest rate swaps or meaningfully influence sovereign bond markets. They trade quantum computing small caps discovered on Twitter, space companies promoted through YouTube videos, Korean semiconductor suppliers circulating through TikTok clips, memecoins trending across Telegram, and leveraged options attached to the most emotionally charged sectors of the market cycle.

This distinction matters because flows concentrated into highly reflexive and speculative areas of the market can create dramatically different trading behavior relative to institutionally dominated markets. Volatility expansions, momentum clustering, reflexive positioning, and narrative-driven liquidity increasingly emerge as defining characteristics of many modern speculative environments, particularly within options markets, crypto ecosystems, and retail-driven equity sectors.

Importantly, this report does not argue that speculation itself is inherently irrational or destructive. Speculative behavior has existed throughout financial history and remains deeply connected to innovation, risk-taking, liquidity formation, and capital allocation. However, the scale, accessibility, social integration, and behavioral optimization of speculation within modern digital systems represents a historically unique environment.

Understanding modern markets increasingly requires understanding this broader societal transformation. The rise of the hypergambling economy reflects more than the growth of gambling applications or retail trading platforms alone. It reflects a structural shift in how modern society interacts with risk, financial aspiration, participation, and opportunity itself.

Conclusion

The modern speculative environment emerged through the convergence of multiple structural forces simultaneously: collapsing technological friction, expanding financial access, rising asset inflation, shifting social norms, and increasingly digital forms of identity and participation. Together, these dynamics transformed speculation from a specialized activity concentrated within isolated environments into a normalized component of everyday life.

The hypergambling economy is therefore not simply the product of gambling applications, memecoins, or social media trends in isolation. It reflects a broader societal transition where financial participation, entertainment, online culture, and speculative behavior increasingly operate inside the same systems optimized for engagement and continuous interaction.

Importantly, this transition did not emerge in a vacuum. It emerged during a period where ownership increasingly outperformed labor, younger generations faced rising barriers to traditional wealth accumulation, and financial speculation increasingly appeared to offer one of the few remaining paths toward asymmetric economic mobility. Under such conditions, speculative behavior increasingly becomes understandable not merely as entertainment, but as adaptation to the surrounding economic structure itself.

Understanding this transition matters because speculative flows increasingly influence not only consumer behavior, but also broader market dynamics, narrative formation, liquidity conditions, and modern volatility structures. Markets themselves are becoming faster-moving, more reflexive, and increasingly shaped by collective attention operating through globally connected digital systems.