Capital Flight

This report presents the view that speculative capital has not disappeared from markets, but migrated between technological narratives and financial regimes. During the 2020-2021 liquidity expansion, crypto became the dominant destination for reflexive speculation as investors chased future internet narratives, decentralized systems, NFTs, memecoins, and increasingly speculative digital assets. Zero rates and abundant liquidity allowed speculative energy to concentrate aggressively across the crypto ecosystem.

The current cycle increasingly resembles that same reflexive behavior, but concentrated within artificial intelligence infrastructure, semiconductors, hyperscaler spending, and the broader deployment of intelligence itself. In many ways, AI-linked speculation today increasingly mirrors the psychology and market structure that once defined crypto during the previous cycle.

Importantly, however, our framework does not view this as a reason to dismiss the AI buildout. Unlike much of the previous crypto cycle, the current AI regime remains tied to real infrastructure demand, visible spending cycles, industrial bottlenecks, and accelerating capital expenditure. As discussed in our previous report, our view on the broader AI infrastructure buildout remains medium to long-term constructive, though highly dependent on liquidity conditions, financing environments, and rates.

At the same time, the collapse of speculative excess across crypto may ultimately prove constructive for the sectors of the industry developing genuine utility. The unwinding of NFTs, ghost chains, memecoins, and unsustainable token structures effectively reset expectations across the broader ecosystem. As speculative attention left the market and the casino emptied, the underlying infrastructure quietly continued developing beneath the surface.

In our view, this may become one of the more important dynamics of the coming cycle.

Stablecoins are increasingly emerging as programmable payment rails. Tokenization is beginning to modernize ownership and settlement systems. Platforms such as Hyperliquid continue demonstrating real demand for crypto-native financial infrastructure, while prediction markets increasingly function as alternative information and risk-pricing systems. Most importantly, the rise of AI agents may create entirely new demand for programmable financial rails capable of autonomous payments, collateral movement, and machine-native economic coordination.

The speculative layer of crypto largely collapsed.

The infrastructure layer survived.

And just as broader market attention has largely moved elsewhere, portions of that infrastructure may finally be approaching meaningful real-world utility.

The Liquidity Regime Shift

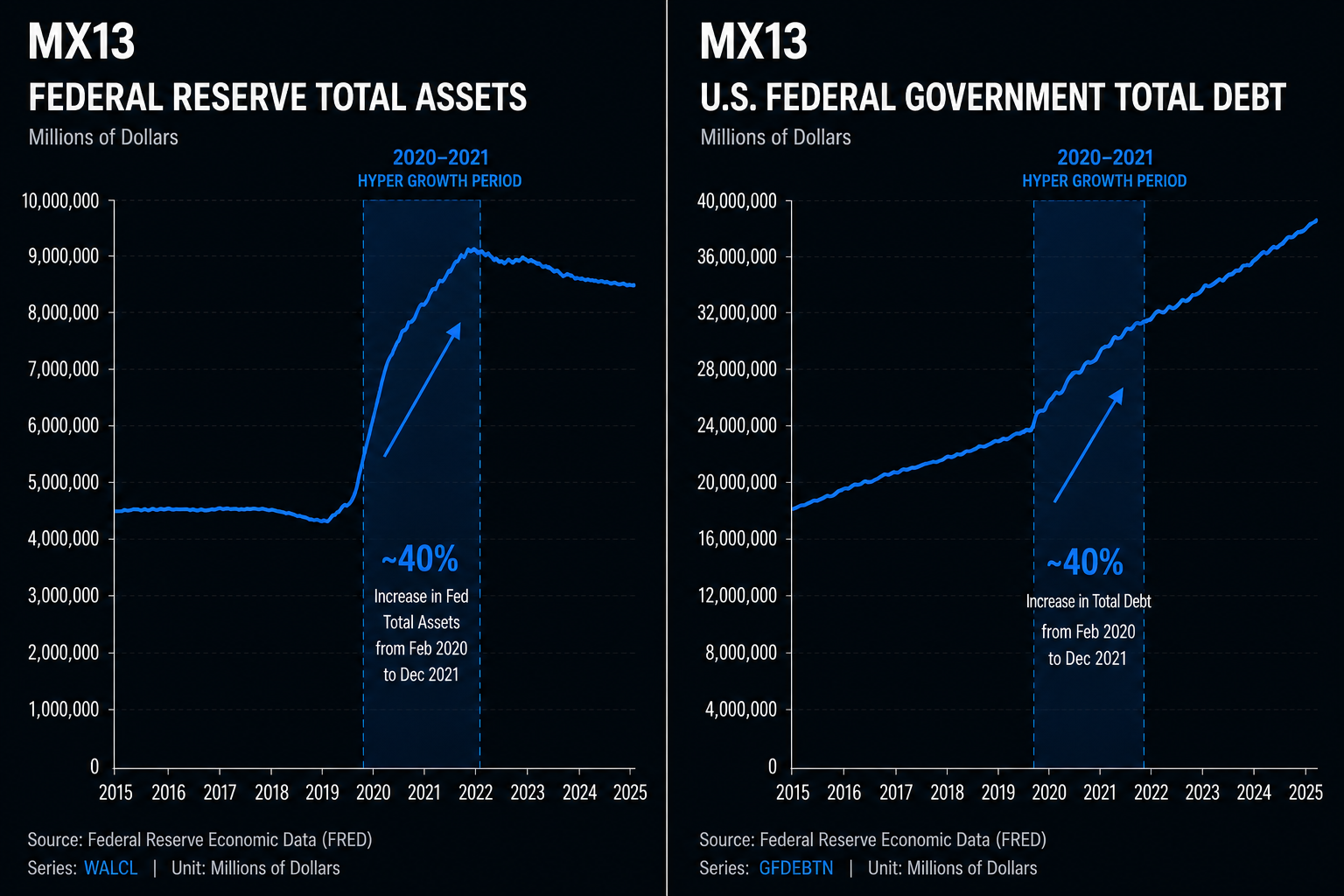

The previous crypto cycle emerged during one of the most accommodative liquidity environments in modern financial history. Real rates moved deeply negative, fiscal expansion accelerated aggressively, and excess liquidity flooded financial markets following the COVID period.

Under those conditions, remaining in cash increasingly became the real risk. Investors were effectively losing purchasing power by staying unallocated while financial assets, technology equities, housing, collectibles, and speculative assets all repriced aggressively higher.

Crypto became one of the primary destinations for that excess liquidity.

Retail stimulus, zero-commission trading, social media reflexivity, and abundant speculative capital combined to create an environment where future technological narratives could absorb enormous amounts of attention and capital. NFTs, memecoins, layer-1 ecosystems, decentralized finance, and increasingly speculative token launches all emerged from that same liquidity regime.

For a period of time, the distinction between technological possibility and economic reality became increasingly blurred. Reflexivity itself became the dominant market driver.

The Exhaustion of the Altcoin Model

As liquidity conditions normalized, many weaknesses across the broader crypto ecosystem became increasingly difficult to ignore.

Large portions of the market became dominated by venture-backed token structures built around inflated fully diluted valuations, aggressive unlock schedules, weak monetization, and fragmented ecosystems competing for increasingly limited attention and liquidity.

The issue was not simply that speculation disappeared. The issue was that many sectors of the market failed to develop durable utility capable of supporting the valuations created during the expansion phase.

Narratives that once absorbed enormous speculative attention increasingly struggled to maintain user growth, liquidity, and relevance once excess liquidity conditions faded. Retail participation declined, volumes compressed, and many ecosystems entered prolonged periods of stagnation.

Much of the debris from that cycle continues weighing on the broader ecosystem today through token unlocks, inflated valuations, fragmented liquidity, and lingering skepticism toward speculative digital assets.

The market moved from expansion to exhaustion.

Speculation Never Dies

Importantly, speculative behavior itself did not disappear.

In many ways, the current AI infrastructure cycle increasingly resembles the reflexive dynamics that once defined crypto markets during 2020-2021. Retail participation, momentum chasing, leveraged positioning, and narrative-driven speculation remain deeply embedded within markets. The venue has simply changed.

Today, speculative capital has increasingly migrated toward AI-linked equities, semiconductors, hyperscaler infrastructure, compute providers, and small-cap companies positioned around the broader intelligence buildout. As discussed in our previous report, the current regime is increasingly centered around infrastructure demand, compute expansion, and industrial bottlenecks tied to artificial intelligence deployment.

The difference is that today's speculation is occurring around visible spending cycles, infrastructure shortages, and real-world industrial demand rather than primarily theoretical adoption narratives.

This distinction matters.

The AI infrastructure regime remains structurally tied to real capital expenditure, earnings growth, and physical deployment cycles. At the same time, however, many of the reflexive behaviors surrounding AI-linked assets increasingly mirror the speculative psychology that once dominated crypto markets.

Markets have not become less speculative.

Speculation has simply migrated.

The Rails Beneath the Market

The periods when markets appear most abandoned are often when future infrastructure quietly continues developing beneath the surface.

Today, crypto sentiment remains broadly exhausted. Retail participation has faded, speculative volumes remain subdued, and much of the market continues viewing digital assets primarily through the lens of the previous cycle's excesses.

Yet beneath that apathy, portions of the infrastructure are beginning to evolve in increasingly meaningful ways.

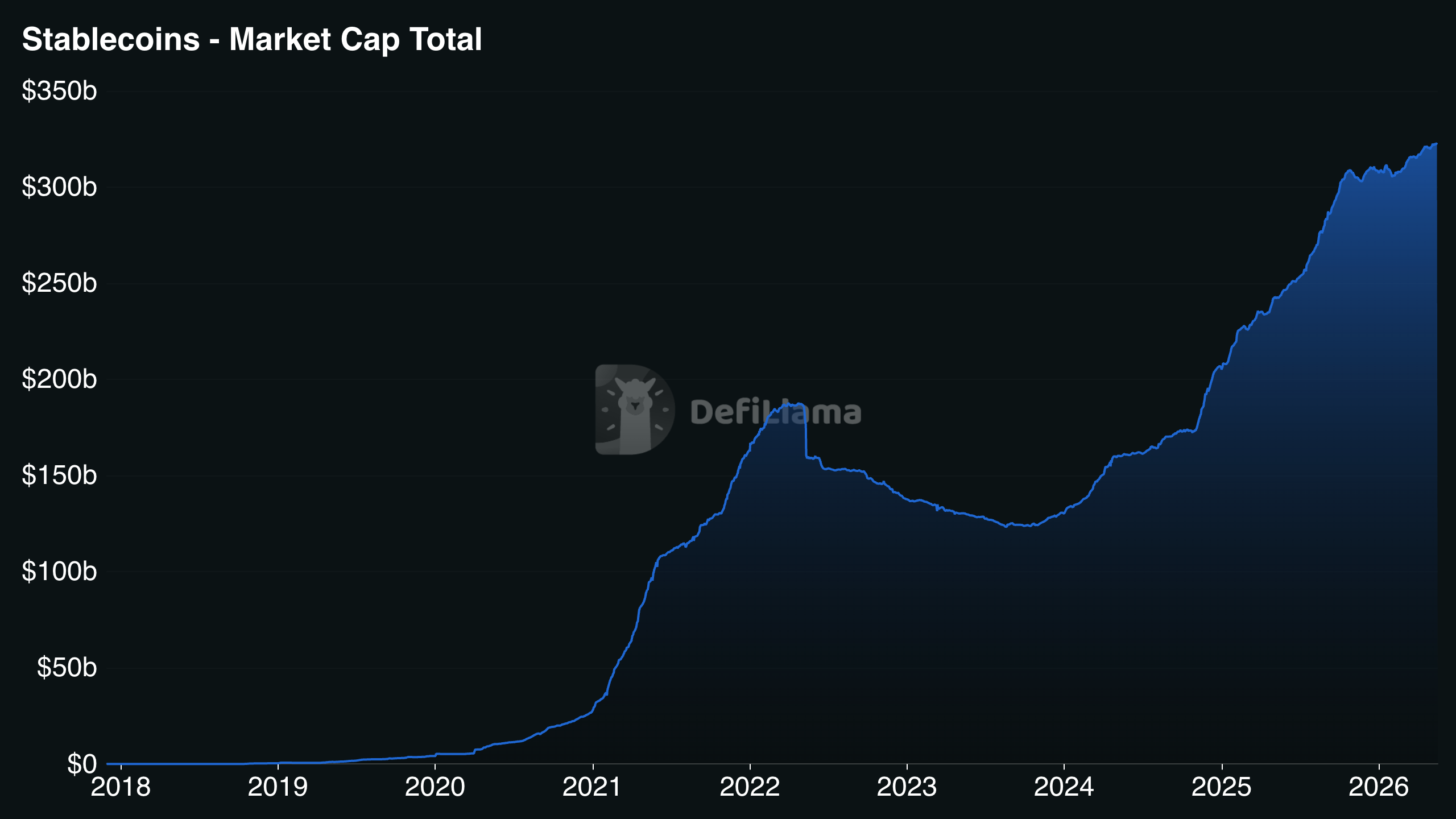

Stablecoins continue expanding rapidly as programmable payment rails, while regulatory frameworks such as the GENIUS and CLARITY Acts move digital settlement infrastructure further into the financial mainstream. In many ways, stablecoins may represent one of the first genuinely scaled crypto product-market fits, allowing capital to move continuously, globally, and increasingly programmatically.

At the same time, platforms such as Hyperliquid continue demonstrating that crypto-native financial infrastructure can still achieve meaningful adoption when paired with strong execution, liquidity, and market utility rather than purely speculative narratives. Prediction markets have similarly continued gaining traction as alternative information and risk-pricing systems during periods where trust in traditional media and polling mechanisms continues deteriorating.

Most importantly, entirely new categories of infrastructure are beginning to emerge around agentic financial systems. As discussed in our previous report on agentic commerce, AI agents increasingly require programmable financial rails capable of autonomous payments, collateral movement, and real-time execution. Early systems such as Tempo represent the beginning of this transition, where crypto infrastructure evolves from speculative assets into machine-native economic rails capable of supporting autonomous digital participants.

In our view, these developments matter far more than many of the narratives that previously dominated crypto markets.

The casino largely emptied.

The rails continued getting built.

In our view, the current environment may ultimately represent the formation of a durable narrative bottom across large portions of the crypto ecosystem.

Not because speculative excess is returning, but because the speculative layer has already largely been flushed from the market.

The reflexive excesses of the previous cycle, NFTs, ghost chains, memecoins, unsustainable token structures, and liquidity-driven speculation, effectively reset expectations across the industry. Retail participation collapsed, attention moved elsewhere, and large portions of the market entered prolonged stagnation.

Yet while speculative attention faded, the infrastructure layer continued developing.

Historically, major long-term opportunities rarely emerge during periods of maximum excitement. They emerge after narratives collapse, participation disappears, and the market broadly stops caring while underlying infrastructure quietly continues improving beneath the surface.

In many ways, 2026 increasingly appears to represent that type of environment for portions of crypto infrastructure.

The Importance of Regime and Timing

At MX13, our framework is not built around blindly chasing whichever narrative currently dominates market attention. Nor is it built around permanently dismissing sectors once speculative excesses unwind.

Markets move through cycles.

The same liquidity conditions that once fueled crypto reflexivity now support the current AI infrastructure regime. Over time, however, all dominant narratives eventually become crowded, consensus-driven, and increasingly difficult environments for differentiated positioning.

This is why our broader framework remains highly sensitive to liquidity conditions, financing environments, and rates. As discussed in our previous report, the current AI infrastructure regime remains deeply dependent on capital availability and broader monetary conditions. Our constructive view on the medium to long-term AI buildout therefore remains conditional rather than unconditional.

At the same time, we believe the market may increasingly be overlooking the significance of emerging crypto infrastructure precisely because broader sentiment remains focused elsewhere. The most important opportunities often begin forming before narratives become consensus and before broader capital fully recognizes where utility is developing.

The challenge is not simply identifying today's dominant narrative.

The challenge is identifying where future utility and future reflexivity may quietly begin forming before broader participation fully recognizes it.

Conclusion

Financial markets continuously rotate speculative energy between narratives, technologies, and sectors. The dominant story of one cycle often becomes the exhausted story of the next, while new infrastructure quietly continues developing beneath periods of weak sentiment and reduced attention.

The current AI infrastructure regime remains powerful. Capital expenditure continues accelerating, infrastructure demand remains significant, and speculative flows continue concentrating around the deployment of intelligence itself.

At the same time, portions of crypto infrastructure may finally be approaching meaningful utility precisely while broader market participation has largely stopped paying attention.

In our view, the most important opportunities often emerge not when narratives appear strongest, but when expectations collapse and the market broadly stops paying attention while underlying infrastructure continues quietly improving beneath the surface.

Our framework therefore remains focused on identifying durable narratives rather than simply chasing whichever sector currently dominates speculative attention. While the broader AI infrastructure buildout remains medium to long-term constructive in our view, we also believe large portions of the crypto sector may increasingly be forming a durable narrative bottom throughout 2026 as speculative excess continues clearing and infrastructure-focused utility begins gradually emerging beneath deeply negative sentiment.