The CapEx Regime

This report presents the view that artificial intelligence is no longer purely a software cycle. While markets continue to frame AI primarily through applications, productivity, and digital services, a much larger structural transition is beginning to emerge beneath the surface. At the center of this shift is the rapid global buildout of AI data center infrastructure. Compute demand is driving an expansion cycle across semiconductors, networking, power systems, cooling, electrical equipment, industrial capacity, and physical construction. In our view, this transition represents a meaningful shift in how capital may be allocated over the coming decade. The defining opportunities may no longer emerge solely from scalable software and expanding margins, but increasingly from the infrastructure required to support the deployment of intelligence at global scale.

NVIDIA CEO Jensen Huang has described this transition as a potential "$90 trillion infrastructure buildout" as intelligence becomes embedded across industries, factories, transportation systems, and national infrastructure. While the exact scale remains uncertain, the broader implication is increasingly clear: AI is evolving from a software narrative into a large-scale industrial and capital expenditure cycle.

The End of the Software-Dominated Regime

For most of the post-GFC period, markets rewarded asset-light business models. Software scaled globally with minimal marginal costs, recurring revenue expanded valuation multiples, and platform businesses absorbed increasing shares of economic activity across entire industries. Investors rewarded scalability, low capital intensity, and long-duration cash flow profiles, producing one of the strongest concentration regimes in modern market history.

A small group of technology companies became dominant drivers of equity performance, benchmark construction, and global capital flows. Software was not simply a sector allocation. It became the organizing principle of the modern investment landscape.

Artificial intelligence begins to alter that structure.

The current cycle is increasingly shaped not just by software adoption, but by the infrastructure required to scale intelligence itself. As deployment accelerates, the limiting factor is no longer simply applications or models. It is the real-world capacity needed to support them.

This changes the direction of capital flows.

The previous decade rewarded companies capable of minimizing capital intensity. The emerging regime may increasingly reward the suppliers of infrastructure, energy, compute, and industrial capacity required to support AI deployment.

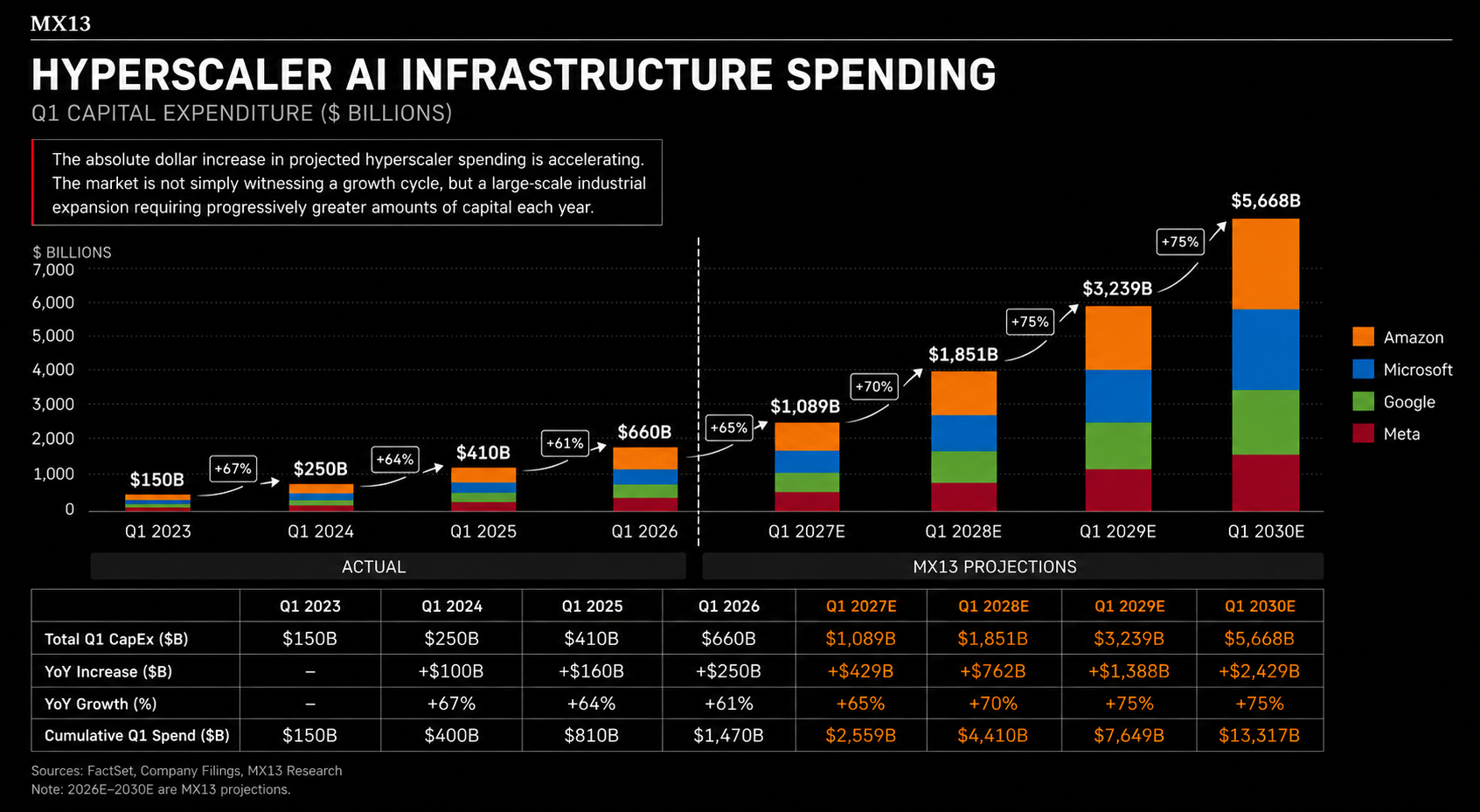

The Data Center Buildout

The current AI cycle is fundamentally being driven by compute expansion. Beneath the applications layer sits a rapidly accelerating global buildout of hyperscale data centers and compute clusters. These facilities increasingly function as the foundational infrastructure layer supporting modern intelligence systems.

As spending accelerates, demand propagates outward across the broader economy. Semiconductors, advanced packaging, optical networking, electrical systems, cooling infrastructure, utilities, industrial equipment, and physical construction all sit downstream of the same deployment cycle. The data center therefore acts as the central transmission mechanism through which AI demand flows into the physical economy.

Importantly, this expansion remains in relatively early stages. Most current infrastructure was not designed for the scale of compute demand now being projected over the coming decade. As hyperscalers, governments, and enterprises continue increasing investment, the physical economy is increasingly being forced to absorb a new class of industrial demand tied directly to intelligence deployment.

The Benchmark Mismatch

Most major benchmarks still largely reflect the winners of the previous era. The largest index weights remain concentrated in companies that benefited from software scalability, cloud adoption, digital advertising, and platform economics. This concentration was rational under the conditions that defined the last decade.

Benchmarks, however, are inherently backward-looking systems. Passive flows allocate capital toward the winners of the previous cycle long before the market fully adjusts to emerging structural changes. Current benchmark construction therefore reflects where capital has compounded historically, not necessarily where the next marginal dollar of investment must flow.

This creates what may become one of the defining investment mismatches of the coming decade.

If AI increasingly evolves into an infrastructure and industrial expansion cycle, then many benchmarks may currently underrepresent the industries positioned directly in the path of accelerating investment. Electrical infrastructure, semiconductor equipment, industrial automation, power systems, networking, cooling, and specialty materials all sit within the supply chain supporting AI deployment, yet many remain secondary allocations relative to dominant software and platform names.

The opportunity therefore may not simply be owning AI broadly. It may instead involve identifying where infrastructure demand and industrial constraints emerge before benchmark weightings fully adjust to the new regime. Increasingly, the market is beginning to recognize that intelligence itself may become abundant while the infrastructure required to deploy it remains comparatively scarce.

Importantly, we do not believe this transition is yet fully understood by the broader market. The continued tendency to frame AI primarily as a software and productivity story may itself suggest the regime remains in a relatively early phase. Structural shifts are rarely obvious while they are occurring. Narratives, positioning, and institutional capital often adapt slower than the underlying economic transition itself.

The Achilles' Heel of the AI Infrastructure Buildout

Despite the strength of the broader AI infrastructure thesis, the current expansion cycle is not without vulnerability. In our view, the primary risk to the regime is not necessarily technological adoption, but financing conditions.

The ongoing buildout of AI infrastructure remains deeply dependent on capital availability, stable liquidity conditions, and the willingness of both private markets and governments to fund long-duration infrastructure projects at massive scale. Data centers, semiconductor fabrication facilities, grid expansion, power generation, networking infrastructure, and industrial automation all require substantial upfront capital investment. The economics supporting these projects become increasingly sensitive as rates rise and financing conditions tighten.

In this sense, rates may represent the Achilles' heel of the current cycle.

Historically, major infrastructure and capital expansion cycles have almost always been created and ultimately constrained by financing conditions. Periods of abundant liquidity and accommodative monetary policy allow capital-intensive buildouts to accelerate, often driving powerful investment booms across both public and private markets. Over time, however, the same forces that enable these expansions can contribute to overheating, inflationary pressures, and tighter financial conditions that eventually slow the cycle itself.

In our view, the current AI infrastructure regime is unlikely to be different.

The same liquidity and financing environment helping fuel the present buildout may ultimately become the mechanism that constrains it. As infrastructure spending accelerates and capital requirements expand, the system becomes increasingly sensitive to rates, credit conditions, and broader monetary policy shifts. Understanding where we are within that cycle may therefore become just as important as understanding the technology narrative itself.

The faster the infrastructure buildout accelerates, the more exposed the system becomes to higher discount rates, rising funding costs, and deteriorating liquidity conditions. A sustained rise in inflation expectations, renewed global tightening cycles, or a disorderly repricing across sovereign debt markets could materially impair the economics supporting portions of the current expansion.

Importantly, many of the sectors leveraged to AI infrastructure trade not only on current earnings, but on expectations surrounding future demand growth and long-duration capital expenditure. As rates rise, the market's willingness to finance and value those future cash flows can compress rapidly. Even structurally strong themes can experience severe volatility when financing conditions deteriorate.

For this reason, we view rates and broader liquidity conditions as critical variables to monitor alongside the AI narrative itself.

Key areas we are closely watching include:

- US Treasury yields and real rates

- Inflation and CPI reacceleration

- Commodity price shocks from geopolitical risk

- Federal Reserve policy and leadership transition risk

- Global central bank tightening cycles

- Credit and financing conditions

- Hyperscaler capital expenditure guidance

- Energy and infrastructure input costs

Importantly, we distinguish between markets pricing a modest reduction in future cuts and the emergence of a sustained tightening regime. Throughout many expansion cycles, rates markets frequently reprice expectations higher without fundamentally disrupting broader risk appetite or capital expenditure trends. The current environment is no exception.

In our view, the more meaningful risk would emerge if repricing evolves beyond forward expectations and into a realized hiking cycle capable of materially tightening financial conditions and reshaping broader market narratives. Historically, major capital expansion regimes tend to remain resilient during moderate rate volatility, but become increasingly vulnerable once liquidity conditions begin tightening in a sustained and realized manner.

Should inflation reaccelerate materially or central banks shift back toward active tightening, we would be prepared to reassess portions of the broader AI infrastructure thesis accordingly.

The broader thesis surrounding AI infrastructure remains constructive in our view, but it is not unconditional. Capital cycles of this scale rarely move linearly, particularly when they become increasingly dependent on financing conditions and long-duration investment assumptions.

Understanding both the opportunity and the vulnerability of the current regime is therefore critical.

Conclusion

Artificial intelligence is often discussed as a continuation of the software era, but the structure of the current cycle increasingly suggests something different. The world is moving from a regime dominated by asset-light scalability toward one increasingly shaped by infrastructure requirements, industrial capacity, and real-world capital expenditure.

Importantly, we do not expect this transition to unfold linearly. Many of the sectors positioned within the AI infrastructure buildout remain highly sensitive to liquidity conditions, financing costs, positioning, and speculative capital flows. As expectations accelerate, periods of crowding and sharp volatility are likely inevitable across both infrastructure providers and broader AI-linked equities.

Our view is therefore not based on short-term price action or the expectation of a straight-line expansion cycle. Rather, we view the current environment through a medium to long-term horizon measured over the coming one to five years. While individual sectors and companies may experience significant volatility throughout that process, we believe the broader direction of infrastructure spending and AI-driven capital expenditure remains structurally higher than what current benchmarks and market narratives fully imply.

The previous decade rewarded margin expansion and digital scalability. The emerging decade may increasingly reward infrastructure providers, industrial capacity, and the receivers of AI-driven capital flows.

The market still largely views AI as a digital story.

Increasingly, it has become a physical one.